At the 11th Tin Industry chain Trading Summit held by SMM in 2021, Li Mingfu, manager of Gejiu Qiandao Metal Co., Ltd., introduced an overview of the global tin market. It is mainly analyzed from the following aspects: the main concentrated places and producing areas of global tin resources, the development of Myanmar tin ore and the cost of imported tin ore varieties, and the future prospect of Myanmar tin market.

Distribution map of global tin resources

At present, there are more than 70 countries (regions) engaged in the exploration, development and utilization of tin resources in the world, and there are 218tin mines in the world, of which 61 have more than 10,000 tons of resources and 16 have more than 100000 tons of resources.

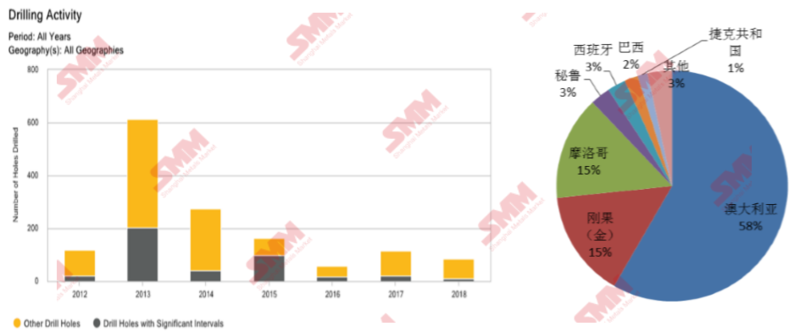

Global tin drilling activities

Global tin resources

The world is rich in tin resources. according to the estimates of the US Geological Survey, the world's tin reserves were 48 billion tons in 2017.

The distribution is relatively concentrated. The reserves of China, Indonesia, Brazil, Bolivia, Australia and Russia rank among the top six in the world, with total reserves of 38.4 billion tons, accounting for about 80 per cent of the world's total reserves.

World tin mine

The main mining tin producing countries in the world are China (44%), Indonesia (17%), Myanmar (13%), Brazil (7%), Peru (5%) and Bolivia (5%). Tin mine production in more than six countries accounted for 91.6% of the world's total output in 2016, with a high degree of concentration.

China: it is the largest tin producer in the world. Since 1993, the output of tin concentrate has been ranked first in the world, accounting for 43.5% of the world's mine output that year.

Indonesia: it is the second largest tin producer and refined tin producer in the world. At present, the production of all tin in Indonesia mainly comes from two companies, Tenma (Timah) and Koba (Koba). Among them, Tianma is the second largest tin production company in the world.

Indonesia's tin reserves stood at 800000 tons at the end of 2016 and can only be supplied for about 12 years at current mining rates. In recent years, due to the decline of tin resource grade in Indonesia, mining enterprises have been forced to turn to underwater mining, the mining cost has increased, and the output of tin ore has been greatly reduced. In 2011, tin production was about 100000 tons, and production has declined significantly since 2012, falling by 24% in 2015 to 68000 tons and 60000 tons in 2017.

The Indonesian government has imposed a total ban on the export of raw metal ores in order to increase the added value of the mining industry. under the influence of new regulations on Indonesian tin export and trading, Indonesia has gained greater price control in August 2013. all exporters are required to trade on the Indonesian commodity and derivatives exchange (ICDX) before export; From August 1, 2015, only refined tin ingots, solders and tinned iron sheets are allowed to be exported, and exporters are required to issue certificates that the exported tin products come from government-registered mines.

According to the latest news, the Indonesian Ministry of Trade has issued a total of 51000 tons of tin export licenses to 12 companies in May 2018. Tianma has received an export license of 32000 tons and can resume shipment in mid-May. Thus it can be seen that the policy has a great impact on the import and export trade of tin mines.

Myanmar: the supply of tin concentrate mainly comes from the WA Manxiang mining area, which accounts for about 95% of the tin supply. After the development of the high-grade and low-cost mine in the WA Manxiang mine, the supply has risen sharply, making Myanmar the third largest supplier of tin mines in the world, from less than 5000 tons in 2012 to 95000 tons in 2016 and falling to 60000 tons in 2017.

Almost all the tin mines in the WA area are exported to China in the form of border trade. Specifically, from 2012 to 2015, the area was mined with high-grade open-pit mining, and the grade of the open-pit mine was even higher than 10% at one time, and the lowest was about 5%. The grade was further reduced to 1.5% and 2% in 2017, and the production cost increased relatively fast. In addition, the difficulty of mining has also greatly increased, because to the low altitude areas after a large number of ore turned to sulphide ore, high temperature, Scald are great problems, resulting in a relatively obvious reduction in ore mining. However, due to the large amount of local mining in previous years, there are more ore stocks in Myanmar, which to some extent supports the production of local tin concentrate. There are also some lower-grade mines, which were not mined below 3% in previous years, and the current price makes the mining of less than 3% economically valuable, and these mines have been mined so that their total tin exports have not declined.

However, the systematic decline of mine grade in Myanmar is inevitable, and the cost of underground mining continues to rise. The decrease in the output of tin mines in Myanmar will directly affect China's tin imports. At present, resources can only support Myanmar's output of more than 50,000 tons for less than three years, which is likely to decline in the future, and no new resources have been found there. The unstable political situation in the WA state of Myanmar will also affect the local tin mining, and there are worries about the supply of tin mines in Myanmar.

Brazil: with the fourth largest output in the world and a large number of high-grade tin deposits, Brazil has the lowest tin mining costs in the world, and most tin mines are profitable even when tin prices are at a low ebb. Brazil's Tin Mine Mountain produced 26000 tons in 2016, the same as the previous year. Parana Panema (Paranapanema) is the main tin production company in Brazil.

Peru: tin mine ranks fifth in the world in terms of output, accounting for 5% of the world's tin output. The Peruvian company Mingsu owns the country's only tin mine, the San Raphael mine, which was once one of the few high-grade mines in the world. However, the problem of declining grade and depletion of resources is becoming more and more obvious.

Peruvian concentrate production has declined year by year in recent years, and tin concentrate production began to decline around 2011. Peruvian Minsu's refined tin production dropped to 18000 tons in 2017, mainly due to the continued decline in tin grade at the San Rafael mine in Mingsu. In contrast, Minsu's Brazilian subsidiary, Topacca, surged 12% to 6600 tons of refined tin in 2017, mainly due to the treatment of more tin tailings.

By the end of 2017, Peruvian tin reserves were about 100000 tons, which could be exploited for about five years.

Other countries: in recent years, most producing countries have been faced with declining grades of existing mines and rising mining costs, such as Malaysia and Bolivia. Although the output of tin mines in Africa (Morocco, Nigeria, Democratic Republic of the Congo), Australia and Brazil may increase to a certain extent in the future, the total output in these areas is relatively low and the impact on China is limited.

Varieties and costs of imported tin ores from Myanmar

Concentrate type

Myanmar tin ores exported to China at this stage: about 50% are flotation ores with a grade of about 30%; about 40% are gravity ores with a grade of 17-18%; and about 10% are gravity plus flotation integrated ores of more than 40%.

Tin mine cost

Tin mine cost = mining right owner (15% Mur25% in kind) + Ministry of Finance tax + concentrator fee + logistics and transportation

Ministry of Finance tax: including in-kind tax (grade higher than 20%) and cash tax (grade higher than 20%).

Mine physical tax: 25% in kind, cash tax is SMM*51%* grade, another 1000 yuan / metal ton road construction fund.

Processing fee of concentrator: the average of raw ore treatment is 280-300 yuan / ton. Therefore, at present, the raw ore grade is about 1%, and only when it is more than 1.3% will a little profit be generated.

Burmese market and policy

Tin mine export requirements are becoming more stringent, on the one hand, reflected in the logistics limit, before the load limit of 60 tons, now 30 tons, and the transport fleet has only 30 vehicles, there will be a shortage of trucks.

On the other hand, it is reflected in the customs procedures for export documents, which requires a longer period, which is extended from the previous 3-day cycle to 7-10 days. In the past, the export company conducted its own sampling and testing for customs declaration, and there was no requirement for impurities; but from April to May, a batch of foreign garbage came into the estuary port, and Yunnan Customs strictly enforced the import policy of goods. now the export of tin ore needs to make an appointment with the customs in advance, and three parties including the quality inspection department, the customs department and the shipper will be arranged for sampling and testing on the spot within three days. Moreover, impurities are now required for lead < 0.5%, mercury < 0.05%, arsenic < 2.5%. If the owner exceeds the standard, the owner needs to write a guarantee.

Future Prospect of Myanmar Tin Market

The output of tin ore decreases gradually, and the mineral processing technology gradually changes from floating first to heavy then floating. This is due to the lower cost of the first weight and then flotation process, which is suitable for low-grade raw ore. The flotation cost is 280-300 yuan / ton, with an average direct yield of 78%; the re-election cost is 80-100 yuan / ton, with an average direct yield of 80%. At present, 70% of the raw ore grade is 1-2%, 30% of the raw ore is more than 2%.

From the point of view of the reagent cost used in the mineral processing process in recent years, because it is entirely imported from China, and the raw ore grade is declining, the reagent cost will gradually increase, which will be one of the main reasons for the increase in Myanmar ore cost.

As the grade of tin ore is getting lower and lower, the cost of tin processing is gradually rising. in order to maintain the pillar industry of the mining industry, the WA Ministry of Finance and the owners of mining rights need to further reduce the tax rate.

Conclusion: due to the epidemic situation and various factors such as production reduction and power restriction, the demand is increased, the resources are limited, the supply is tight, the import uncertainty is great, and the tin mine price rises for a long time.

![Lack of Clear Guidance on the Geopolitical Situation, Repeated Swings in Macro Sentiment Put Futures Under Pressure Again [SMM Tin Midday Commentary]](https://imgqn.smm.cn/usercenter/wRltl20251217171750.jpg)